Bayfront Infrastructure Capital IV

Bayfront Infrastructure Capital IV Pte. Ltd. (“BIC IV”) is Bayfront’s fourth offering of Infrastructure Asset-Backed Securities (“IABS”) that was priced in September 2023. BIC IV issued 4 classes of rated Notes that are listed on the Singapore Exchange, an unlisted and unrated mezzanine Class D tranche that is guaranteed by GuarantCo Ltd, and an unrated equity tranche that is 80.5% retained by Bayfront and 19.5% held by the UK FCDO through its MOBILIST programme. BIC IV offers investors exposure to a pre-assembled portfolio of project and infrastructure loans and bonds issued by borrowers in Asia Pacific, Middle East, the Americas and Africa.

Just like its predecessors BIC II and BIC III, the BIC IV transaction once again featured a dedicated sustainability tranche, in the form of the Class A1-SU Notes, backed by eligible green and social assets as defined in Bayfront’s Sustainable Finance Framework. The Class A1-SU Notes are considered as Secured Sustainability Standard Bonds under ICMA Green Bond Principles 2021 (with June 2022 Appendix 1), Social Bond Principles 2023 and Sustainability Bond Guidelines. The Class A1-SU Notes have also been recognised by the Singapore Exchange for meeting recognised standards for green, social or sustainability fixed income securities.

Investor Relations

Offering Document

Moody’s Rating Reports

Payment Date and Investor Reports

Audited Financial Statements

Issuance

Five Classes of Notes

The Class A1 Notes, Class A1-SU Notes, Class B Notes and Class C Notes are rated by Moody’s and listed on the Singapore Exchange. The Class D Notes are unlisted and unrated, and are guaranteed by GuarantCo Ltd (rated A1 by Moody’s and AA- by Fitch).

80.5% of the Preference Shares are held by Bayfront as Sponsor of the transaction, while the remaining 19.5% are held by the UK Foreign and Commonwealth Development Office, as part of its Mobilising Institutional Capital Through Listed Product Structures (MOBILIST) programme.

| Class | Amount Issued (US$ million) |

Amount Outstanding3 (US$ million) |

Issue Ratings (Moody’s) |

Spread5 | Legal Maturity Date | |

|---|---|---|---|---|---|---|

| Original | Current | |||||

| A1 | 170.6 | 154.2 | Aaa (sf) | Aaa (sf) | 150 bps | 11-Apr-2044 |

| A1-SU | 115.0 | 104.0 | Aaa (sf) | Aaa (sf) | 142.5 bps | 11-Apr-2044 |

| B | 54.5 | 54.5 | Aa1 (sf) | Aa1 (sf) | 225 bps | 11-Apr-2044 |

| C | 31.6 | 31.6 | A3 (sf)4 | A3 (sf) | 490 bps | 11-Apr-2044 |

| D1 | 13.0 | 13.0 | Not rated | Not rated | 350 bps | 11-Apr-2044 |

| Pref Shares2 | 25.6 | 25.6 | Not rated | Not rated | N.A. | |

1 The Class D notes are guaranteed by GuarantCo Ltd for principal and interest amounts payable

2 Retained and not offered. Bayfront holds 80.5% and MOBILIST holds 19.5% of the Preference Shares

3 As of 11 April 2024

4 The Class C tranche was initially rated Baa1(sf) at launch of the transaction (as seen in the Moody’s Pre-sale Report), and was subsequently upgraded to A3 on issue date due to the tightening of the final spreads for the Class A1-SU, B and C tranches

5 Spread is applied over 6-month daily non-cumulative compounded SOFR

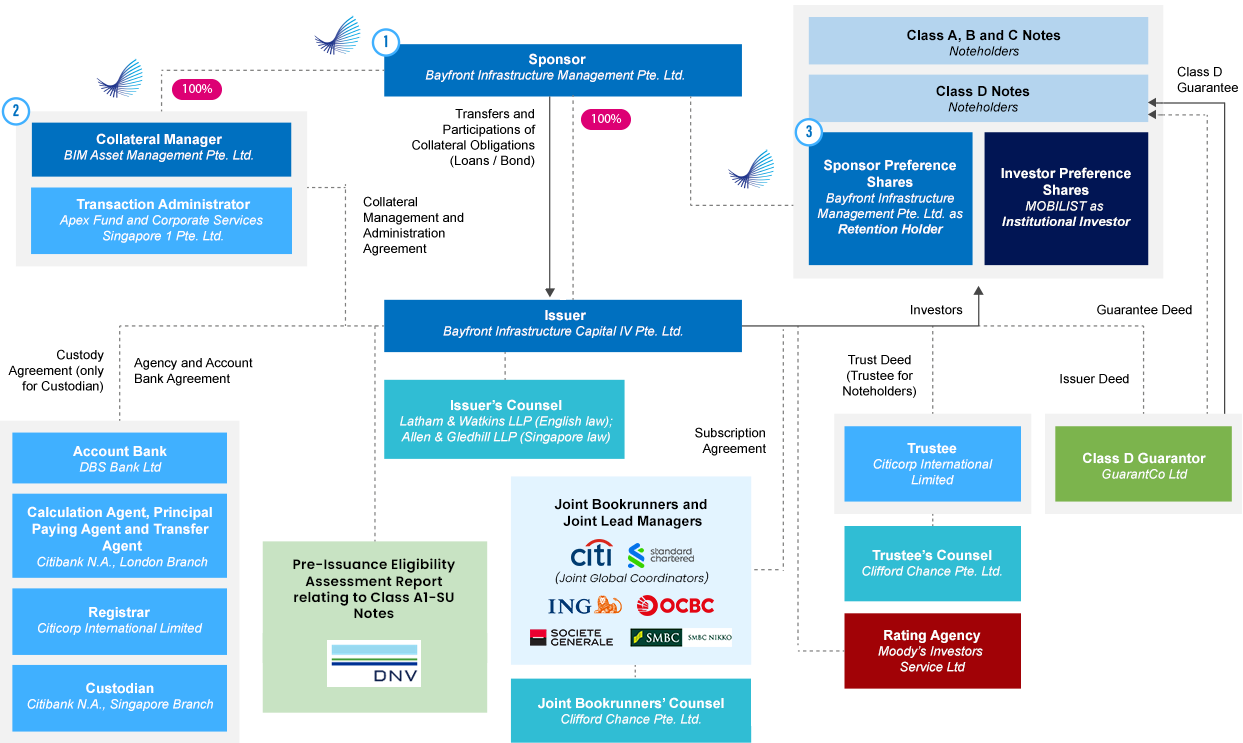

Key Transaction Parties

Bayfront is the Sponsor for BIC IV.

As Sponsor, Bayfront was responsible for:

- sourcing of the Portfolio from the Originating Banks and executing loan/bond transfers, including initial screening, credit analysis, due diligence and documentation;

- liaising with credit rating agencies to obtain credit assessments on the portfolio assets and credit ratings for the Class A1, A1-SU, B and C notes (“Rated Notes”); and

- leading the structuring and execution of the transaction, including resourcing arrangements, investor marketing and distribution, together with the Joint Global Coordinators and Joint Bookrunners.

BIM Asset Management Pte. Ltd. (“BIMAM”) is the Collateral Manager for BIC IV.

As Manager, BIMAM is providing certain investment management, administrative and advisory functions for BIC IV which includes:

- managing and monitoring the performance of the portfolio assets;

- maintaining credit assessments on the portfolio assets and credit ratings of the Rated Notes;

- handling any replenishment and disposition of the portfolio assets (if required);

- handling all voting requirements, consents, amendments, modifications, waivers or any other notices for the portfolio assets;

- providing information available to the Transaction Administrator and ensuring that the Transaction Administrator operates the Priority of Payments and reporting requirements in a timely and accurate manner;

- providing management services including periodic investor reporting, treasury, compliance and budgeting requirements (in conjunction with the Transaction Administrator); and

- acting as primary interface with investors, banks, borrowers, multilateral financial institutions, export credit agencies and other stakeholders, including investor relations.

Apex Fund and Corporate Services Singapore 1 Pte. Limited is the Transaction Administrator for BIC IV, performing portfolio administration and reporting services. Citicorp International Limited is acting as Trustee and DBS Bank Ltd. as the Account Bank.

The Issuer (BIC IV) is a wholly owned subsidiary of the Sponsor (Bayfront). Bayfront holds all of the ordinary shares and also holds 80.5% of the preference shares, with MOBILIST holding the remaining 19.5% of the preference shares.

Transaction Features and Highlights

- 40 project and infrastructure loans and bonds across 33 projects in Asia Pacific, the Middle East, the Americas and Africa

- 15 countries of project and 10 industry sub-sectors

- Renewable energy as the largest single sub-sector at ~30%

- 83.5% of the portfolio at inception relates to operational projects, while the remaining 16.5% relates to projects in advanced stages of construction and which benefit from appropriate credit mitigants, such as sponsor completion guarantees or sponsor support

- 48.7% of the portfolio at inception are investment-grade assets, with a Moody’s Rating Factor of 610 (Baa3) or lower (based on Moody’s existing credit estimate disclosure policy introduced in March 2022, which no longer incorporates the benefit of external credit support for loans covered by export credit agencies or multilateral financial institutions)

- Stringent review and credit approval processes – firstly by the originating banks, an any export credit agencies and multilateral financial institutions providing credit support, and secondly by Bayfront as part of its due diligence process when acquiring the loans/bonds as sponsor

- Detailed analysis undertaken by credit rating agencies to assign credit estimates for each underlying loan (and public rating for the single project bond in the portfolio)

- Alignment of interests with Bayfront acting as the sponsor and majority (80.5%) investor in the first-loss tranche

- Deep portfolio management expertise, with BIMAM acting as the collateral manager for BIC IV, and also acting as the collateral manager for the BIC III transaction (issued in 2022), the BIC II transaction (issued in 2021) and as sub-manager on the BIC transaction (issued in 2018 and called in 2022)

- Static pool with limited replenishment rights within a 3-year replenishment and 3-year non-call period

- Offtake agreements with reputable and creditworthy counterparties

- 78.7% of the portfolio involves project borrowers that need to maintain minimum debt service coverage ratios as one of their financial covenants

- Natural FX and interest rate hedge – US$-denominated and floating rate SOFR-based assets and liabilities

- 29.9% of the Notes issued are to be fully allocated to a portfolio of eligible green and social assets that meet the eligibility criteria stated in Bayfront’s Sustainable Finance Framework

- 33.4% of the portfolio at inception relates to green assets (renewable energy projects and energy efficient data centres), enhancing BIC IV’s green footprint from the previous BIC II and BIC III transactions

Overview of the Portfolio

The Portfolio is diversified across 40 project finance and infrastructure and bonds, spread among 10 industry sub-sectors, and located in 15 countries across Asia Pacific, the Middle East, the Americas and Africa. The Portfolio is backed by 33 projects with stable and predictable long-term cash flows, including through offtake agreements entered with reputable and creditworthy counterparties including major global corporates, state-owned enterprises and government or government-linked sponsors.

The Portfolio has been assembled with a focus on availability-based infrastructure assets in the renewable energy and conventional power and water subsectors, while also including assets from other sub-sectors, subject to strong credit metrics and pre-set concentration limits put in place by Bayfront. Accordingly, Bayfront believes that the diversification within the Portfolio is a significant mitigant to geographical, industry or corporate and consumer business-cycle risks.

By Country of Project

Based on geographical project location

By Country of Risk

Based on ultimate source of payment risk

By Sector

By Credit Enhancement

By Ratings Distribution1

1 As calculated by Bayfront using Moody’s Rating Factors based on Moody’s previous credit estimate disclosure policy that incorporates the benefit of external credit support for loans covered by export credit agencies and multilateral financial institutions.

By “Deep” Emerging Markets Exposure2

2 Defined as countries rated Ba3 and below by Moody’s. Includes Bangladesh and Jordan

ECA = Export Credit Agency; NHSFO = Non-Honouring of Sovereign Financial Obligation guarantee, provided by the Multilateral Investment Guarantee Agency (MIGA, member of the World Bank Group); PRI = Political Risk Insurance provided by MIGA

By Commodity Price Exposure

Based on ultimate source of payment risk

By Construction Risk

Based on ultimate source of payment risk

Portfolio Selection Principles

The following are the key selection principles that Bayfront has applied in selecting and constituting the Portfolio:

Structure and Sourcing

- Sourced from 12 leading international and regional commercial banks

- Focused on projects in Asia-Pacific, the Middle East, the Americas and Africa that are operational or in advanced stages of construction, but which benefit from appropriate credit mitigants, such as completion guarantees

- Material portion supported by export credit agencies, multilateral financial institutions and project sponsors through various forms of credit enhancement (e.g. guarantees and insurance)

- Focused on availability-based infrastructure assets

- High and moderate carbon intensity oil and gas sub-sectors (comprising LNG and gas, Floating production, storage and regasification, Other oil and gas, energy shipping) and metals and mining sub-sectors subject to concentration limits

Cashflows

- US$-denominated floating rate assets, reflecting the US$ payment profile for interest and principal on the Notes issued

- Fixed loan/ bond repayment schedules providing certainty on cash flows

Sustainability Tranche

Just like its predecessors BIC II and BIC III, the BIC IV transaction also featured a dedicated sustainability tranche, in the form of the Class A1-SU Notes, backed by eligible green and social assets as defined in Bayfront’s Sustainable Finance Framework. The Class A1-SU Notes are considered as Secured Sustainability Standard Bonds under ICMA Green Bond Principles 2021 (with June 2022 Appendix 1), Social Bond Principles 2023 and Sustainability Bond Guidelines.

- 29.9% of the Notes issued are to be fully allocated to a portfolio of eligible green and social assets that meet the eligibility criteria stated in Bayfront’s Sustainable Finance Framework

- 33.4% of the portfolio at inception relates to eligible green assets (renewable energy projects and energy efficient data centres), enhancing BIC IV’s green footprint from the previous BIC II and BIC III transactions.

DNV Business Assurance Singapore Pte. Ltd. has provided a sustainability bond pre-issuance eligibility assessment on the Class A1-SU Notes.

Asset Pool by Original Loan Commitments

| Green Use of Proceeds | Asset Category | USD (mln) |

|---|---|---|

| Solar Energy Projects | Renewable Energy | 14.606 |

| Wind Energy Projects | Renewable Energy | 26.873 |

| Hybrid Renewable Energy Projects1 | Renewable Energy | 51.403 |

| Run-of-River Hydro Projects | Renewable Energy | 4.691 |

| Data Centre Projects | Energy Efficiency | 15.000 |

| Social Use of Proceeds | Asset Category | Social Benefit | Target Population | USD (mln) |

|---|---|---|---|---|

| Desalination Investments | Affordable Basic Infrastructure | Climate resilience – Drinking water supply | Residents of Qatar and Kuwait | 17.051 |

| Transportation - Roadway | Affordable Basic Infrastructure | Interconnection of lower socioeconomic areas with urban areas | Residents along the corridor supported by the highway in a Southeast Asian country classified as a Developing Member Country by Asian Development Bank | 14.300 |

| Total | 143.924 |

1 Hybrid projects with a combination of (i) solar and wind energy; or (ii) solar and wind energy and battery storage.

Investor Profiles

By Investor Type

By Geography

Not for distribution to any person or address in the United States.

This website, and our social media sites, contain information which is for information purposes only. They do not constitute an offer nor an invitation nor a recommendation to subscribe to or to purchase, to hold or sell securities, nor is the information contained herein meant to be complete or to serve as a basis for any kind of obligation, contractual or otherwise. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, reliability, accuracy, completeness or correctness of such information. The information is not intended to provide and should not be relied upon for tax, legal or accounting advice, investment recommendations or a credit or other evaluation regarding the securities of Bayfront Infrastructure Capital IV Pte. Ltd. or its affiliates (collectively, “Bayfront”). Additionally, third-party information distributed on our social media sites may not represent our views and unless otherwise expressly indicated, we take no responsibility for, nor do we endorse, any such information.

Any information memorandum posted up on this website is being provided as a historical, reference source only and is not being used, and no one is authorized to use, disseminate or distribute it, in connection with any offer, invitation or recommendation to sell or issue, or any solicitation of any offer to purchase or subscribe for, securities.The information memorandum is current only as at its date and such availability of the information memorandum on this website shall not create any implication that there has been no change in the affairs of Bayfront since the date of such information memorandum or that the information, statements or opinions contained therein is current as at any time subsequent to such date. Bayfront is under no obligation to update any information memorandum. An information memorandum may contain forward-looking statements and these statements, if included, must be read with caution as set forth in the section "Forward-looking statements" in such information memorandum.